As we cross the threshold of 2026, the global financial ledger is being rewritten not in ink, but in the heavy, immutable luster of bullion. The opening months of the year have been defined by a sharp, jarring discord; on February 28, the escalation of conflict in West Asia—ignited by US-Israeli strikes on Iran—sent a tremor through the markets. Yet, the reaction was not the simple, linear “flight to safety” we have been conditioned to expect.

In a world defined by shifting alliances and the weaponization of finance, the traditional rules of the game are being fundamentally redesigned. We find ourselves at a sophisticated crossroads: the security of ancient metals is clashing with the modern volatility of a surging U.S. dollar, creating a landscape where the most seasoned investors are asking a singular, curiosity-driven question: why are the “safe-haven” rules of the last century suddenly being rewritten before our eyes?

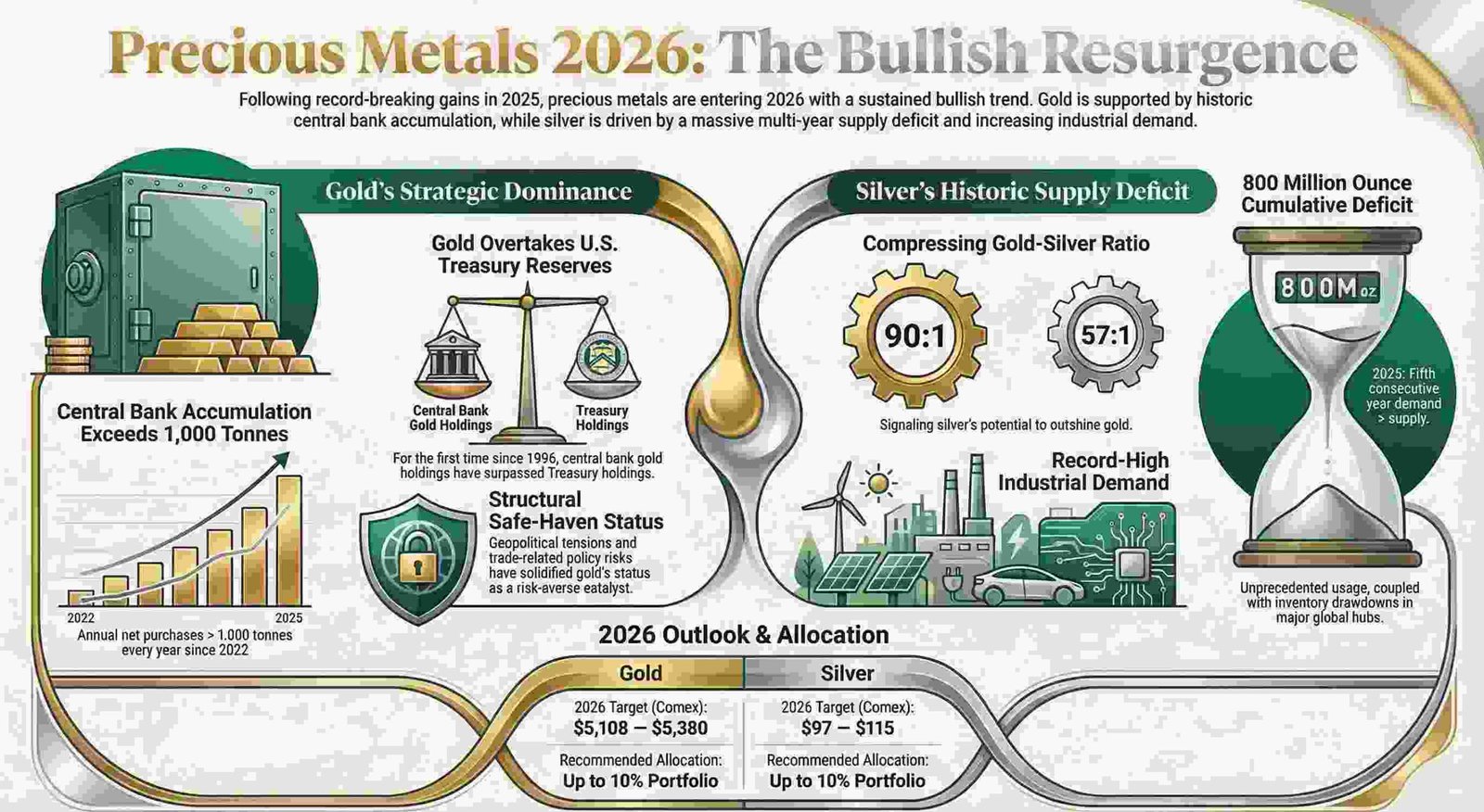

The Great Reserve Flip: Gold Overtakes the U.S. Treasury

A structural metamorphosis is currently unfolding within the world’s most guarded vaults. For the first time since 1996, foreign central banks have prioritized gold reserves over U.S. Treasury holdings. This is no mere seasonal fluctuation; it is a fundamental reorganization of global wealth and a strategic retreat from USD-denominated debt.

The catalyst for this shift is deeply geopolitical. Central banks have internalized a “lesson learned” from the freezing of Russia’s reserves—a move that proved paper assets are only as secure as the political goodwill behind them. For the sophisticated investor, this institutional hoarding creates a “structural floor.” As nations pivot toward assets with zero counterparty risk, they provide a permanent base for prices that transcends retail volatility.

“For the first time since 1996, foreign central banks’ gold reserves have overtaken their U.S. Treasury holdings. Persistent gold accumulation, rising U.S. debt risks, and an accelerating diversification away from U.S. assets are driving a structural shift in reserve composition toward hard assets.”

Silver’s Secret Supercycle: The 800-Million-Ounce Deficit

While gold often commands the headlines of the financial press, it is silver—the “white metal”—that possesses the more aggressive sparkle in 2026. We have emerged from a historic five-year supply deficit cycle (2021–2025) that has left the global market parched. The cumulative shortfall has reached nearly 800 million ounces, a staggering figure that is roughly equivalent to a full year’s worth of global mine production.

The most compelling narrative, however, lies in the “Gold-Silver Ratio.” After stretching to an eclipsed 90:1 in early 2025, the ratio has compressed sharply to approximately 57:1. Technical benchmarks suggest a gravity-defying pull toward the historical 50:1 and even 40:1 levels. At a 40:1 ratio, silver would comfortably exceed the $110 mark, making it the breakout asset of the decade.

The Curated Drivers of the Silver Rally:

- The Scarcity Factor: A completed five-year deficit cycle leaving inventories at historic lows.

- Industrial Vitality: Record-high demand in green technology and electronics outpacing mining output.

- Inventory Drawdowns: Persistent depletion of stocks in major global hubs, specifically London and China.

- Strategic Designation: The U.S. classification of silver as a “critical mineral” and China’s tightening export restrictions.

- Monetary Tailwinds: Federal Reserve rate cuts reducing the opportunity cost of non-yielding hard assets.

The War Paradox: Why the “Safe Haven” Stumbled

Since the onset of the West Asia conflict on February 28, gold has behaved with a frustrating complexity. Typically, war triggers an immediate, unyielding price surge. However, in mid-March, the “yellow metal” met the “War Paradox.” While geopolitical anxiety was at a fever pitch, a stubbornly strong U.S. dollar acted as a massive headwind.

Because bullion is denominated in dollars, the currency’s strength made physical gold prohibitively expensive for international buyers, effectively dampening demand at the very moment safety was most desired. This reflects the complexity of 2026 markets: a “safe haven” is only as accessible as the currency used to buy it. This friction eventually drove a pivot, as investors began looking for more liquid, digital ways to capture the trend.

The Digital Gold Rush: ETFs Outpace Equity

In a landmark shift for retail sentiment, particularly within the Indian market, a new hierarchy of investment has emerged. For the first time, investors are funneling more capital into Gold ETFs than into traditional equity mutual funds. This represents a profound “digitization” of risk aversion, where the aesthetic of wealth meets the efficiency of the smartphone.

This shift is woven into the cultural fabric of the current festive cycle. As Eid, Ugadi, Gudi Padwa, and Navratri approach, we see a sophisticated bifurcation in how the metal is consumed:

- 24-Karat Gold: The standard of purity, now used almost exclusively for digital holdings and strategic investment.

- 22-Karat and 18-Karat Gold: The artisan’s choice, remaining the bedrock for the creation of intricate jewelry for traditional celebrations.

The $5,000 Horizon: Where the Bull Trend Ends

The technical outlook for the remainder of 2026 remains unapologetically bullish. Technical strategists point to a “technical continuity” following the record-breaking advances of 2025. With falling yields and sustained institutional demand, the path of least resistance is upward.

Current price milestones for the 2026 horizon include:

- Gold: Analysts have identified a key resistance level at 5,108**, with a secondary target of **5,380.

- Silver: Milestones are set at 97**, **103, and a peak of $115—contingent on the gold-silver ratio gravitating toward the 40:1 historical norm.

This is not a short-term speculative bubble, but a calculated realignment of value. The “unprecedented buying spree” by central banks is a long-term strategy designed to weather a decade of fiscal uncertainty.

“Central banks have maintained a strong appetite for gold, with annual net purchases exceeding 1,000 tonnes every year since 2022. This unprecedented buying spree is primarily driven by strategic diversification away from the US dollar and a desire for safe-haven assets.”

Conclusion: The 10% Rule and the Road Ahead

The evidence suggests that the bullish cycle for precious metals is far from exhausted. While domestic headwinds—such as potential government shifts in import duties—may create short-term price fluctuations, the structural foundation is historically strong.

Expert consensus currently recommends a 10% portfolio allocation to precious metals as a necessary hedge against currency debasement and geopolitical volatility. As the world’s central banks trade paper promises for the permanence of gold and silver, the private investor is presented with a clear roadmap.